With no interest and explicit repayment schedules, Afterpay (ASX: APT) has epitomised millennial behaviour and presented a simple product that gives consumers greater control over their credit spend. The “buy now, pay later” platform has witnessed immense growth and seems to be at the start of its life cycle.

APT’s product success has seen it become a verb in our everyday conversation. For many of us, we FaceTime, Google, and now it seems that Afterpay is becoming the verb for “buy now, pay later” services.

Despite its incredible reception by consumers, there is increasing commentary citing concerns that current regulations do not adequately protect consumers from the potential harm of these services.

In October, the Senate called an inquiry into the alternative credit and financial service industry, including services like APT. Whilst it may be reasonable to assume that regulation poses a threat to APT’s business model, ECP Asset Management (ECP) investigated what it would mean going forward and the impact this will have on the business.

Our investment case for APT allows for a scenario where the National Consumer Credit Protection Act 2009 (NCCP) incorporates “buy now, pay later” services. Our research suggests this may not be a negative for APT. In fact, we would go as far as to suggest that these regulatory requirements may even improve APT’s competitive position by creating greater barriers to market entry.

What Regulation Means

APT does not fall under the definition of a credit provider. APT extends credit for periods less than 62 days without charging fees or interest, assuming timely payments. If the regulation evolves to incorporate “buy now, pay later” under a broader definition, what changes would APT need to implement?

Current regulation requires credit products to obey strict lending requirements. The provider needs to have a credit licence and must participate in an external dispute resolution scheme. APT currently meets both requirements.

Additionally, APT needs to decide whether a credit contract is suitable for each consumer by conducting a comprehensive credit report (CCR). This requires:

- Making reasonable inquiries about the consumer’s financial situation, requirements and objectives; and

- Taking reasonable steps to verify the financial situation.

Regulatory Compliance Is Manageable

Conducting a CCR would require an adjustment to APT’s sign-up process. However, this will have a limited impact to the consumer experience and will be relatively inexpensive to implement.

CCR’s can be conducted online, and at scale. Credit reports can be ordered through credit bureaus, such as Equifax, while income and expense verification can be executed through tools such as Yodlee. This is a well-worn path and can be easily implemented by APT.

Our research indicates that credit checks would be immaterial and cost less than $2 per customer application. If APT is legally required to perform a retrospective credit check of their customer base, it’s likely a small, immaterial cost of $4–5 million will be incurred.

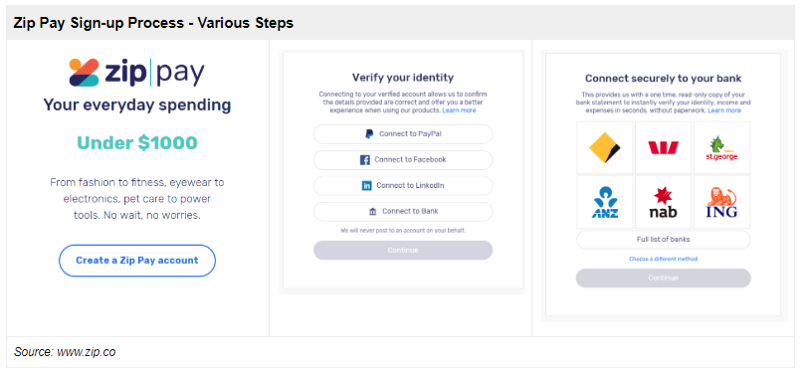

Zip Co Case Study

Zip Co (ASX: Z1P), the company behind Zip Pay, provides some clues as to how APT’s process may evolve. Z1P’s management team have developed a sign-up process that’s likely to be compliant in an environment in which “buy now, pay later” products are regulated. Zip Pay performs an identity check, credit check and income and expense verification before making an approval decision.

We recently tested the new sign-up process and found it to be a seamless experience that’s completed with approval in under four minutes. Zip Pay’s recently adopted application process is the same as the Zip Money product application, which is already a fully regulated credit product.

We believe the implementation of a similar process for APT is realistic and easily achievable. As indicated in a recent market announcement by Z1P:

“The company conducts a credit and identity assessment, including a credit bureau check on every applicant … In recent times, the company has introduced real-time income and expense verification into the Zip Pay application process. Were products such as Zip Pay to become regulated, there would be little or no disruption to the business.” — 18 October 2018

Can Regulation Improve APT’s Competitive Position?

The lack of application friction has historically been a driver of APT’s adoption in Australia. Added regulation may slow down the rate of new domestic applicants by adding more friction points (scraping bank accounts, income verification, etc) to the sign-up process. For us, it seems penetration has hit critical mass, and the late adopters of the product will be less resistant to additional checks than earlier ones.

That said, it is conceivable that application frictions resulting from a required CCR could become a competitive advantage for APT in Australia.

New entrants in the “buy now, pay later” space will face an uphill battle in establishing a network effect while they attempt to build consumer and merchant relationships. Further, APT’s current merchant offering, brand power and consumer loyalty is a valuable differentiator when compelling consumers to complete a more comprehensive application process.

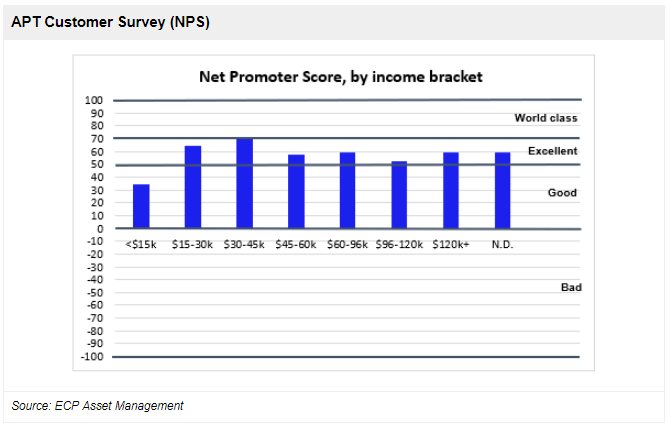

This view is supported by our own proprietary consumer survey we conducted which found that APT had an extremely high Net Promoter Score (NPS) across all income brackets.

Central to our forensic research process is generating exclusive insights and collecting independent data to inform our investment hypothesis. We do this to ensure that we are able to connect our qualitative assessment to the reality of the numbers. High-quality, growth investing requires a conviction in the key factors driving future growth.

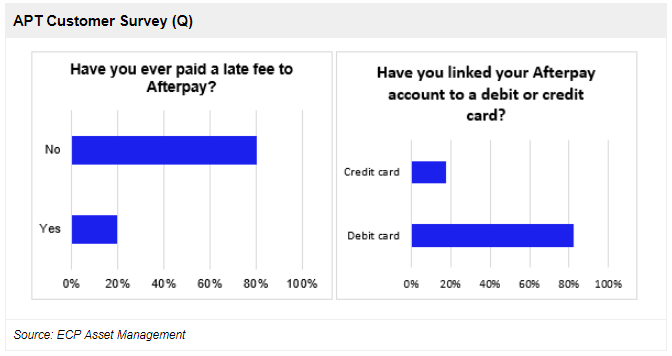

In the case of APT, management has consistently indicated that a low portion of orders triggers a late fee (10%), only a fraction of consumers have ever incurred a late fee (22%), and few consumers link their account to a credit card (15%). These statements were consistent with our consumer survey findings.

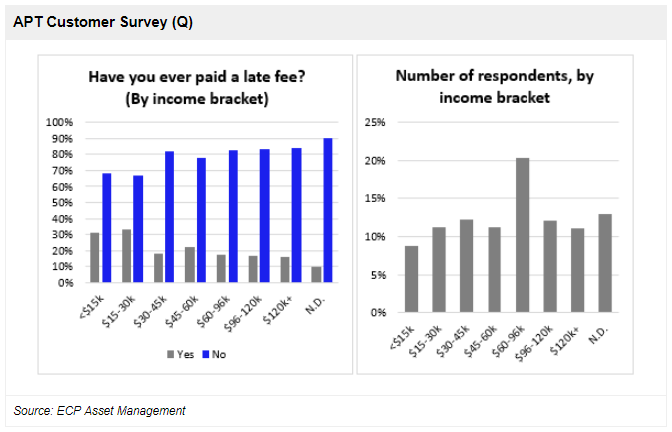

When breaking down instances of late fees in our survey by income bracket, we found marginally more late fees were paid by lower income cohorts. However, these same customer cohorts recorded a Net Promoter Score for APT ranking either ‘good’ or ‘excellent’. In this light, it is worth considering why APT rates so positively with consumers.

Product Attributes Drive Adoption

For any company, acquiring 2.8 million customers in three years is incredible. So what’s different about APT?

We define APT’s product success factors as simplistic and free.

- Simplistic - The four equal repayments over a fixed time-frame means consumers have a simple repayment model. This model cannot extend and there are no variable repayment schedules. Any missed repayments will mean account suspension. These product factors remove many layers of necessary self-discipline that come with traditional credit cards. This resonates strongly with consumers.

- Free - If repayments are made on time, APT is a free credit product for consumers. Further, APT’s terms and conditions for retailers explicitly prohibit them from adding back the merchant fee to the consumer at checkout.

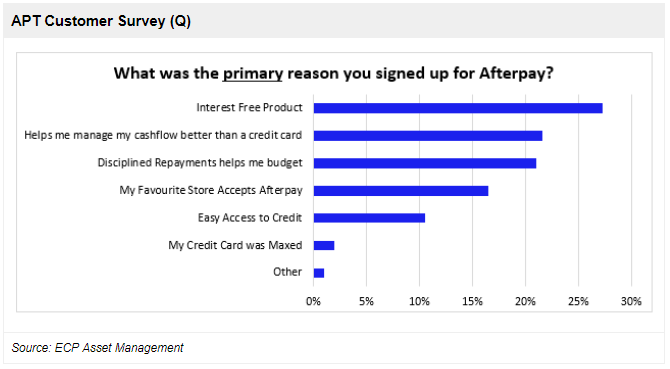

Our views are validated by our consumer survey which indicates the most common reasons for adoption relate to the interest-free product, combined with the in-built repayment discipline required to be a continuing customer of APT.

Is There A Risk Existing Customers Aren’t Creditworthy?

APT’s model is unique. It starts small, allowing customers to “earn” their own capacity by displaying appropriate repayment behaviour. APT’s model implicitly tests customer creditworthiness through time before scaling up the credit limit it will approve.

If the regulator required APT to conduct a retrospective credit check on existing customers and determine if its credit contract is suitable, we believe the number of customer accounts “at risk” would be low.

APT previously indicated that 75% of its customers have an outstanding balance less than $350, while 90% have an outstanding balance less than $500. Given the small credit balances outstanding, there is a very low likelihood that a material portion of APT’s customer base is not “creditworthy” for an account.

Independent survey work disclosed by APT earlier in the year showed that its customers under-index among low income cohorts across Australia. Separately, ECP’s consumer survey indicated that 68% of APT customers had credit card debt less than $1,000, whilst 42% had no credit card debt at all. In contrast, RBA and ASIC statistics indicate that the average consumer credit card debt is nearly $4,200 of which $2,600 is accruing interest.

We believe these factors are strong indications of a customer base that is not seeking additional credit, but a customer base that is more interested in managing their finances via alternative means.

What’s Next?

ASIC is reviewing the “buy now, pay later” segment with an initial report expected to be released in December 2018. The report is set to outline whether further regulation of the sector is necessary.

For our investment case, we assume that regulation may be extended to cover “buy now, pay later” providers, however, regulation is not certain. Some alternatives include granting ‘product intervention powers’ to ASIC, which allow the regulator more influence over financial products outside current the NCCP definition.

The New Zealand regulator recently reviewed the segment under their Credit Contracts and Consumer Finance Act (CCCFA), and decided that given limited evidence of consumer harm, and the protection under the Fair Trading Act, further regulation was not required at this time.

Conclusion

Long-term investing requires a deep understanding of a company’s business model and potential threats putting the model at risk. Regulation is often a factor to consider, especially within the financial services industry.

In this case, we believe APT regulatory risks appear to be misunderstood. Any regulatory evolution that includes APT and its peers under a broader definition of credit will have a limited impact on business operations, its future growth potential, or profitability.

The article has been prepared by ECP Asset Management Pty Ltd. ECP is a funds management firm based in Sydney, Australia.. For further information visit www.ecpam.com. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for financial advice. ECP owns shares in Afterpay Touch Group Ltd. ABN 26 158 827 582, AFSL 421704, CAR 441986.

Featured Articles