Challenger Limited (ASX: CGF) is a quality franchise, but one that is not without risk. At ECP we are constantly revisiting previous investment ideas as the modern business environment is constantly changing as industries evolve, businesses build competitive advantages, and various milestones are met. Challenger is a business we have reviewed many times; it meets our criteria of a quality franchise, it creates value for its clients, achieves an adequate return on equity, and has a dominant market share with a large growth runway ahead.

As a high conviction fund manager with a focus on capital preservation, we need to sleep at night knowing our portfolio companies have capital structures built to withstand all economic conditions. In this instance, despite an exciting growth opportunity ahead, we fail to find conviction in the safety of Challenger’s capital structure. For this reason, we continue to watch from the sidelines, believing it is better to sleep well than eat well.

Background

Challenger’s main business is the provision of annuities, with a growing focus on its lifetime product. A lifetime annuity is an insurance designed to give the buyer an adequate income stream for the remainder of their life. A buyer pays Challenger a lump sum upfront, and in return is promised a fixed or inflation-adjusted income stream for life.

Challenger invests this upfront lump sum to generate a return which partially covers the committed income stream to be paid to the client. It makes money when at the end of the client’s life, the lump sum has not been fully depleted. If the client outlives expectations or the original upfront sum is depleted, Challenger loses money and must utilise its balance sheet to continue funding the client income stream.

Attractive Growth Drivers

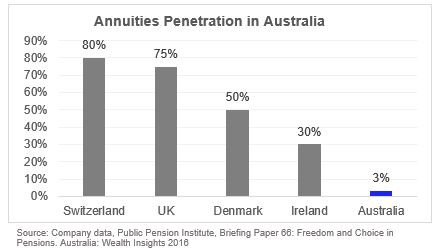

Challenger is the dominant player in Australian annuity products with ~77% market share [1]. Despite the unique ability to serve a critical retiree need, product penetration is very low in Australia. A 2015 industry study indicated that low Australian adoption is due to (1) the age pension provides some mitigation against longevity risk; (2) the superannuation system has focused on the attainment of savings rather than the provision of retirement income; and (3) a perception that annuities present poor value for money [2].

Nonetheless, lifetime annuities are continually growing in acceptance as advisor/client product understanding improves and product distribution via wealth platforms increases. Increasing penetration from a low base, combined with an aging demographic underpin a structural tailwind for new annuity sales over the long-term.

New Regulations Would Accelerate Annuity Sales

In May 2018, the Australian Government released its ‘Position Paper’ proposing a plan for a better retirement income framework. The paper noted that the current superannuation system is under-developed and needs to be better aligned to the objective of providing perpetual retirement income that supplements the Age Pension. This change may provide the catalyst that accelerates lifetime annuity sales.

The Government put forward its proposed principles for a Comprehensive Income Product for Retirement (CIPR), a concept first raised in a discussion paper in 2016. The report stated “it is not sufficient for the CIPR to provide income only to life expectancy. The trustee would need to ensure that the CIPR is designed in such a way that even if the member lives to 105, they will continue to receive broadly the same level of income from the product.”

Notably, the paper suggested that a CIPR would require a (minimum) 15–20% allocation to lifetime income product, with the proposal to legislate the covenant by July 2019, for commencement from July 2020 [3]. This could significantly increase the demand for lifetime annuities.

ECP estimate there will be ~$120 billion per annum in superannuation assets transitioning from accumulation to pension phase across the next decade.

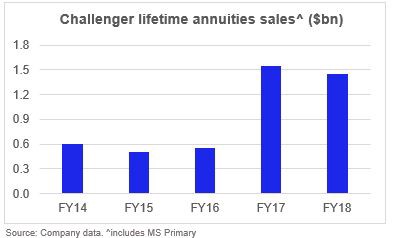

If we assume 50% of transitions are impacted by the CIPR — excluding SMSFs, lump-sum payments and low balance super funds — and apply the minimum 15% allocation to the (proposed) lifetime income products, this could create $9 billion in annual new demand for lifetime annuities, compared to Challengers ~$1.5 billion annual sales today [4].

Significant Opportunity Up For Grabs

Our analysis of Challenger’s unit economics for lifetime annuities indicates they are priced on a ~3% nominal rate of return (IRR) [5]. If we assume Challenger can generate a 4% IRR on its lifetime annuity sales, then every $1 in lifetime annuities sold creates $0.08 of net present value.

This means that the potential $9 billion per annum of new demand for lifetime annuities could create $700 million in net present value every year, a material opportunity when compared to Challenger’s dominant market share and $5 billion market cap.

But Caution is Prudent for Equity Investors

To ensure Challenger can meet its client promise in all market scenarios, it is regulated by APRA and must hold a minimum level of regulatory capital at roughly 13% of life assets [6]. To give shareholders a safety buffer, Challenger holds nearly 20%. This means it can lose up to 7% of its $19.2 billion life assets before breaching APRA’s minimum capital requirements; a buffer necessary to prevent Challenger being forced to raise equity at discounted prices, potentially in cycle troughs, impairing existing shareholder value.

As a high conviction fund manager with a focus on capital preservation, we need to sleep at night knowing our portfolio companies have capital structures built to withstand all economic conditions. The critical question is: “do we have conviction that Challenger won’t lose more than 7% of its investment portfolio?”.

A Look at the Numbers

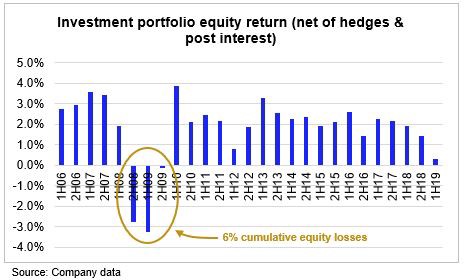

As a starting point, we estimate Challenger’s portfolio equity return in the 2008 financial crisis saw cumulative losses of -6%, net of portfolio hedges [7]. If we exclude the +4.8% saved by hedges across this period, underlying portfolio losses were -10.8%.

These net losses, in the context of the previous crisis extremities, give some comfort that Challenger’s 7% buffer is adequate protection into the future in most economic scenarios.

However, it appears that a decade defined by low credit market yields has forced Challenger to step outward on the risk curve in order to find an adequate yield to meet its return on equity targets. As a consequence, portfolio quality appears to have decreased over time.

Challenger’s investment portfolio is 65% allocated to fixed income. Within this, the quality mix since 2012 has shifted lower with non-investment grade credit now comprising 23%, up from 14%, and the lowest investment grade rating (BBB) now represents 24% of the portfolio, up from 15%. In contrast, AAA-rated assets used to be 24% of the book but now only represent 13%.

As a consequence of a lower quality fixed income book and reliance on hedging to manage downside risk, we find it difficult to have conviction that Challenger’s investment portfolio will perform within tolerable levels in future downturns.

Conclusion

Challenger has a significant opportunity ahead, but the risk-return trade-off remains our key concern. A decade of low credit market yields has created challenges for the company to deploy its client capital in a means by which it can continue to price annuities attractively and meet its return on equity targets, all whilst minimising future risk to equity holders.

As a high conviction fund manager, ECP only invests when we have a high degree of conviction on all the long-term growth, return and risk factors in our portfolio companies. We believe it’s important to understand both the narrative of an investment and the numbers that support it; including the requirement to understand the downside potential.

Footnotes: [1] Strategic Insights, September 2018; [2] Australian Journal of Actuarial Practice, Volume 3, 2015: Australia’s piece of the puzzle — why don’t Australians buy annuities?; [3] Super Funds would not be required to offer a CIPR until July 2022; [4] FY18 reported; [5] Male, enhanced income (no liquidity), non-inflation adjusted, $100,000 annuity with $6,552 annual income from age 65 to assumed death at age 86; [6] Varies, dependent on asset allocation; [7] Post interest payments to clients.

Disclaimer: The article has been prepared by ECP Asset Management Pty Ltd. ECP is a funds management firm based in Sydney, Australia. ABN 26 158 827 582, CAR 441986 AFSL 421704. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for financial advice. For further information visit www.ecpam.com.

Featured Articles