Decisions made by central banks around the world have drastically impacted equity markets. Globally, many asset owners would never have predicted the extent of the rise in interest rates, with many grumbling at the lack of foresight provided by key decision-makers. When dealing with change events that were not foreseen, investors have few tools to prepare and manage these associated risks. Probabilistic modelling cannot fully encapsulate these black swan events, and for equity investors, taking a resilience-based approach may better protect their wealth against unknown uncertainties and risks.

The Reserve Bank of Australia (RBA) had fallen foul of prior statements that they would not raise the cash rate until 2024. Phillip Lowe, Governor of the RBA, recently apologised for people listening to what was said and acting on that rather than paying attention to the caveats of what was said. This apology was clearly in response to gripes similar to the one made by a dear friend who said, “the people who should know better have totally misled us all, and now I have lost a small fortune.”

Phillip Lowe has since insisted that his guidance was never “calendar-based” but “state-based”, meaning the path of future rate hikes was always tied to the state of the economy, not some predetermined date in a diary. However, would our client have borrowed as much money if he had thought rates might rise sooner than 2024? I think not.

Policy Frameworks

The Governor was not alone in his view on future interest rate movements, with similar opinions espoused by other central banks. In 2015, the Executive Office of the US President published insights into the premise on which interest policy is based, highlighting how interest rates are determined.

Through the lens of Economic Theory, the paper explores the Ramsey model, which generates a fundamental link between per capita consumption growth, the real interest rate, and the economy’s growth rate.

The paper starts with the simplest version of the model and then, in a later discussion, considers uncertainty but still utilises the standard Euler condition and standard functional forms for household preferences to arrive at the formula 𝑟𝑡+1=𝜌+𝜎𝑔𝑡+1, with the real interest rate defined as a function of the growth rate of consumption per capita.

The discount rate r measures how much people value current consumption relative to future consumption. The intertemporal elasticity of substitution, 1/σ, measures the extent to which households are willing to give up consumption today for consumption tomorrow. If growth is expected to be high, people will try to borrow against their future higher income to consume more now, which will drive up the interest rate.

At some point, the higher interest rate will discourage borrowing and restore equilibrium between the return on capital investment (which reflects the ability to produce income in the future) and the household’s desire to consume now. The interest-rate response depends on the interaction between σ, and the growth rate of per capita consumption and is developed from modelling historical data.

The report concludes:

In a world with financially integrated national capital markets, the general level of world interest rates is determined by the equality of the global supply of savings and global investment demand.

- Capital markets of advanced economies are now tightly integrated, while emerging market economies are becoming increasingly integrated into the global financial system. Low-income economies remain partially segmented from the global capital market.

- As a consequence of increasing international market integration, long-term real and nominal interest rates are increasingly moving in tandem and have declined along with U.S. rates. Nominal interest rates also tend to be correlated across countries though differences in inflation expectations can produce differences in nominal rates.

- In a world with uncertainty, global long-term real and nominal interest rates will include risk premiums that can reflect country-specific risk factors. Strong economic linkages, however, reinforce substantial correlation in countries’ long-term bond risk premiums.

Here, the final point highlights one key issue for investors: uncertainty. Risk frameworks have long acknowledged the role of uncertainty, with many theoretical models highlighting the distinct roles of risk and uncertainty. Importantly, uncertainty represents more about economic activity than risk.

Uncertainty is Unpredictable

Uncertainty relates to unpredictable events that result in adverse outcomes. For many investors, applying probabilistic-based modelling to portfolios can adequately manage the trade-off between risk and return. While risk can be determined by probabilities, uncertainties cannot.

When determining our expectations of the future world, we do so based on the current information at hand. The difference between objective and subjective probabilities is that the former relates to risk (known outcomes), while the latter relates to uncertainty (unknown outcomes).

Investors have to make subjective assessments of the future states of the world — we do not have objective probabilities. Here, the difficulties lie in which subjective assumptions are made and how they are applied.

Since uncertainty relates to our knowledge of what is to come, the effects of this uncertainty cannot be precisely detailed. As Donald Rumsfeld noted, these are the ‘unknown unknowns’, which are the uncertainties of where “we do not know what we do not know”.

After the Global Financial Crisis and following the Lehman Bros collapse, Alan Schwartz, the CEO of Bear Stearns (which ran into trouble before the bailout of Lehman Bros), said, “we all !@#$% up… banks, regulators, everybody… and fifty years from now, there’ll be another crisis, and it’ll be about some instrument that we’ve never heard of.” Well, as it turns out it wasn’t fifty years, it was ten years, and it wasn’t an instrument, it was COVID-19.

In 1952, Milton Friedman and Leonard Savage presented their expected-utility paper, commenting that even when you do not have enough information for objective probabilities, you should better adopt some probabilities and make decisions under them. This seems similar to what resulted in the announcements regarding interest rate movements.

When assigning subjective probabilities, one does not know with certainty the outcome in advance as there is no such evidence. In uncertain situations, the errors may be so significant that attempting to predict these outcomes is unhelpful.

The Resilience Defence

There is no risk in steady-state environments, yet when we find ourselves in situations of change, risks will emerge. For investors, change increases risk because we do not know its effects, leaving open the possibility of unexpected consequences or outcomes.

Traditional risk management practices lie in the domain of probabilities, while non-probabilistic assessments rarely feature in risk mitigation methods.

Black swan events occur at unpredictable intervals. Nissim Taleb, the author of 'The Black Swan: The Impact of the Highly Improbable', highlighted the concept of black swan events, commenting that these events are low in predictability and high in impact.

The spread of COVID-19 and the Ukraine war profoundly affected global equity markets. Stock markets fell due to the increased uncertainty, and the immediate impact these events had on economic activity saw reduced trade, lower investment and household spending, and rising employment — all of which contributed to the first recession in over 30 years.

Over the long term, unexpected situations arise that may not be incorporated into probabilistic modelling. These situations may (negatively) impact investment portfolios and, when left unmanaged, may seriously affect long-term wealth. By accounting for these ‘unknown unknowns’, investors will better protect and grow their wealth through time.

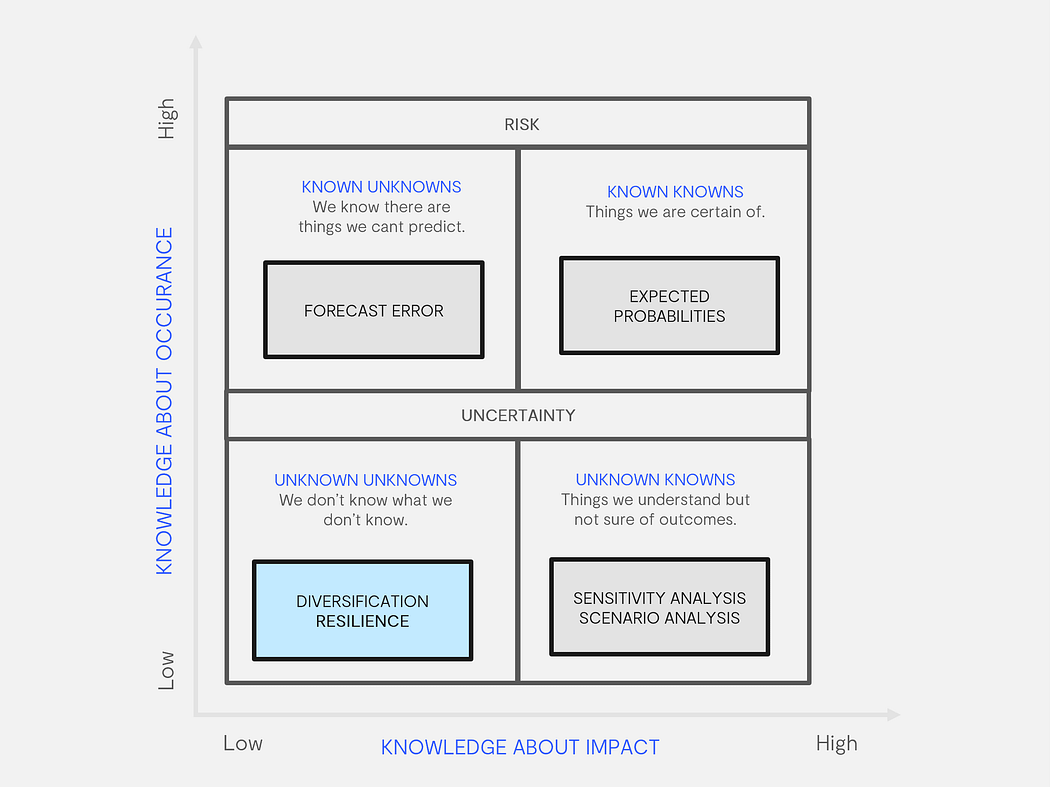

Below outlines the concepts of risk and uncertainty, highlighting the known-unknown continuum, which highlights two fundamental criteria: knowledge of the occurrence and knowledge of impact.

Academic theory suggests several approaches when faced with the ‘unknown unknowns’, including diversification which has been relied upon by many investors worldwide. However, diversification too often is but an excuse for poor due diligence.

In situations where non-probabilistic risk management is required, investors must take a different approach — resiliency. Incorporating resilience into risk management frameworks is what we do at ECP and means we can use these heuristics to guide non-predictive decision-making under uncertainty.

As investors, we are essentially business owners. Finding resilient companies means investing in those that can grow their economic footprint while strengthening their competitive advantage despite rare, unforeseen events.

Resilient companies are well-resourced (financially and organisationally) to withstand ‘unknown unknowns’. A key component of determining resilience is the concept of Dynamic Capabilities (DC). At ECP, we use the DC framework to gauge and assess a firm’s ability to manage, react and grow in times of uncertainty. See Sustainability Analysis & Resilience.

DC’s are essentially change-oriented capabilities that help firms redeploy and reconfigure their resource base to meet evolving customer demands and competitor strategies. Not all firms have this ability, and the best businesses have this dynamic capability.

When a firm has a Sustainable Competitive Advantage (SCA), its strategic approach has found a recipe that creates value that only belongs to the firm, where imitation is impossible. However, an SCA is not sustainable forever, as the resources driving its competitive advantage may change due to externalities.

Prepare for 2023

Investors are loss-averse, not risk-averse. When investing over long-term horizons, risk management strategies need to account for the unforeseen risks that may lead to capital loss. Resilience is the preferred approach to diversification.

Investing over the long-term means investing in a careful, considered and committed way. Being conservative in one’s optimism means being squarely focused on mitigating the risks of the inevitable black swan.

We know with certainty that rare events will occur and that the intensity of these is unknown. Investors applying probabilistic-based approaches to risk management frameworks will only partially account for these looming disasters. Applying resilience-based principles will mitigate the dormant risks lurking behind these major disruptions.

Even a one-in-two-hundred-year storm has been known to have occurred two years in a row, and it is our job, as portfolio managers, to ensure that the companies in our portfolio can withstand our ignorance of future outcomes, especially as the frequency of its occurrence is unknown.

It is said that life can only be understood backwards, but it must be lived forwards. You can’t connect the dots looking forward, and for now, all we can hope for is that we do not have another black swan event soon and that we all have a peaceful Christmas with our family and friends and we all return to work at the end of the holidays revitalised and refreshed.

From the entire team here at ECP, thank you all for your ongoing support. We wish you and your families a Merry Christmas and a happy and healthy New Year.

Manny

Featured Articles