Scaling Square from inception to a US$150bn payments business with multiple layers of protection wrapped around its profitability was only part one of Block’s success story. Below we explore how Block took learnings from scaling Square and is actively building an enormous US consumer fintech called Cash App.

Cash App was created in 2013 at an internal company hackathon as a way for consumers to make electronic peer-to-peer payments. Its creators were looking for an easy way for people to split bills at a restaurant or transfer money to friends and family, a simple-sounding service made difficult by the Byzantine US consumer banking system.

At the time, the ability of Cash App to build a network of users seemed unlikely. Venmo (now owned by PayPal) was already an established peer-to-peer platform, while Google launched its peer-to-peer functionality. Arguably, the opportunity for a late entrant to scale shouldn’t have existed.

Despite the obstacles, Cash App has reached 80 million annual active users and is dominant across nearly half of the US. How it got there is a story of first-class execution across product and marketing.

Cash App Comes To Life

The initial product release in 2013 — then named Square Cash — was a simple way to quickly send money over email, allowing users to avoid navigating the traditional banking system, which often involved physically lining up at the local bank branch.

A user would enter a dollar amount in the subject line, address the email to the intended recipient, and CC a Square-designated email. The receiver would access the cash by creating a Square account with a linked debit card.

To enhance usability and simplicity, the company released a mobile application — renamed Cash App — in 2014 and introduced a new identity mechanism called the ‘$cashtag’ in 2015, which allowed users to make payments to one another without needing the recipient’s email address or mobile number. Cash App also expanded to businesses which were able to create profiles and accept payments for a small fee.

The company’s critical insight was that despite the existence of Venmo at the time, no service existed that would guarantee to make these money transfers ‘instant’, rather than waiting 2–3 days for transferred funds to clear through the banking system. By using its balance sheet, Square was able to launch an ‘instant transfer’ service for a small fee, and customers loved it.

Cash App’s initial stronghold was developed in the Southeast of the US as word spread amongst underbanked consumers about the easy-to-use, fast and free money transfer service. A continually improving customer experience allowed the peer-to-peer nature of its money transfers service to unlock self-reinforcing customer growth, as early adopters started inviting family and friends into the network, typically by sending money to them via the app. Reaching one million active users in 2015, Cash App proved its concept had a competitive edge and a right to exist.

Cash App Goes Viral

Block then set out to build Cash App’s scale by leveraging its ‘edge’ — a superior customer experience and a user-led viral growth strategy. The company exploited a social trend, which became known as ‘Cash App Friday’, where users would make personal appeals for money to each other on social media along with their $cashtag. In 2017, Cash App jumped on the trend.

Rather than marketing through traditional online channels (Google and Facebook) to acquire customers, the company participated directly in Cash App Friday — incentivising app downloads by giving money to customers either directly or via A-list celebrities and influencers. In one example, Travis Scott tweeted that he was giving away $100,000 to fans via Cash App. The tweet received over 120,000 replies.

There were other surprising aspects to Cash App’s virality, such as music creators referencing Cash App in their lyrics. It was clear the product and brand resonated strongly with users. Cash App invested in amplifying this resonance, financially supporting and partnering with artists, and tying back into the viral-social media marketing initiatives.

The brand strategy to fuse Cash App with parts of the American subculture allowed it to soften the edges of its money-related app, similar to how Square positions its brand in contrast to the typical highbrow, financial institution.

The growth strategy proved successful and drove a doubling in reported active customers every year from 2015, reaching a scale of 15 million in 2018, with the cost to acquire a new transacting customer a mere $5.

Enhancing Competitive Sustainability

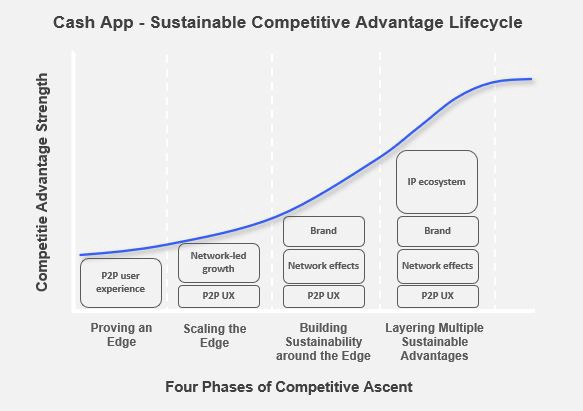

With micro-network effects amongst its users driving growth and its unique brand becoming established, Cash App began building stronger hard-to-copy and non-substitutable elements around its business to enhance its competitive sustainability.

Early on, Cash App progressively developed a stronger IP ecosystem by rolling out features to increase utility for consumers, aligning with its mission to “make the world’s relationship with money more relatable, instantly available, and universally accessible”.

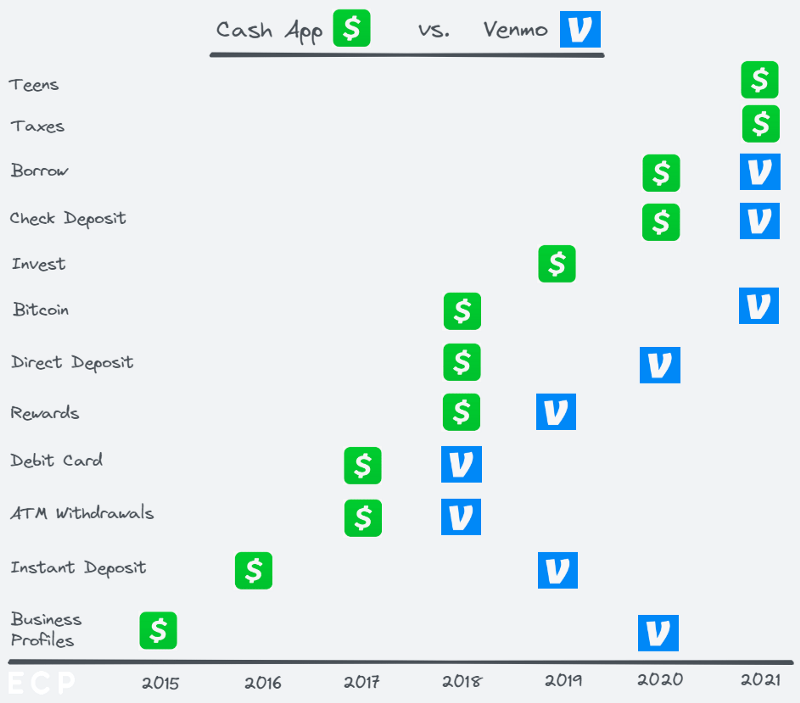

Starting in 2016, Cash App rolled out features beyond peer-to-peer payment functionality. It offered the ability to store funds in the app and launched the Cash Card to enable ‘spending’ by its users. This led Cash App deeper into the East and West Coast markets, with strong adoption amongst millennials.

In 2017 the company released custom physical debit cards, which allowed ATM withdrawals. The ability to take direct deposits into Cash App (paychecks and tax refunds) was launched in 2018 along with the ‘Boosts’ rewards program (product discounts partially funded by merchants), followed by fractional stock and bitcoin trading.

The biggest benefit from the company’s fast development cadence became evident during COVID-19. As the economy locked down in March 2020, the US Government announced stimulus checks which would be immediately available for citizens with bank information on file with the IRS for tax purposes. The problem, however, was that ~14% of Americans with income under $40k did not have a bank account, and many did not earn enough to file tax returns. Upon receiving a stimulus check, many would need to rely on expensive cash checking services to access their money.

By April, the IRS launched a tool for US citizens without a historically filed tax return to access stimulus funds directly. Hours later, Cash App responded by launching a feature which gave users a routing and account number (essentially mimicking a traditional bank account) to allow direct access to government stimulus payments. This meant that users didn’t need to sign up for a traditional bank account or wait for a check in the mail.

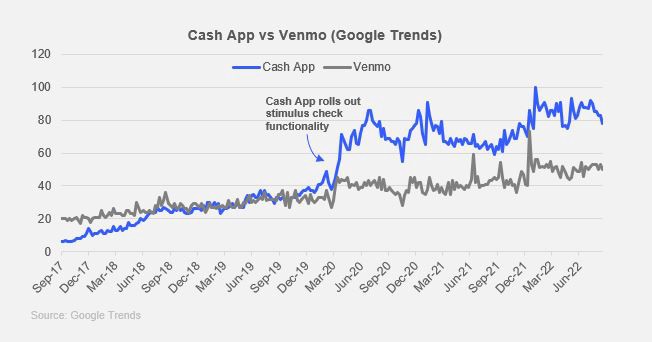

The agile product development unlocked massive user growth as the peer-to-peer nature of Cash App’s user base spread the word about the app’s growing utility. Cash App rocketed past Venmo for the first time in search popularity adding 12 million new monthly active customers in 2020, reaching 36 million by year-end.

Constantly Leading Innovation

Cash App has continually proven itself as the innovation leader amongst its peers. In what we see as an underappreciated move, Block launched Cash App for Teens in late 2021. On the surface, this is a smart way for Cash App to expand its market size and move early on the under-served 13–18 years market.

At a deeper level, it provides Cash App with a sharper spearhead into Venmo’s geographic stronghold by establishing user relationships earlier in their life. These younger users then onboard family members as part of their setup process and early money management circles, sparking new networks and proving Block understands how to leverage network advantages better than most.

It’s not difficult to imagine Cash App going one step earlier in customer lifecycles, launching ‘Kids’ as a sub-account under parental custody to educate kids about money using tools like weekly chore lists and custom interest rates to encourage savings goals.

Nearly a year later (at the time of writing), Venmo is yet to protect its turf and respond with its own Teens launch. Nevertheless, we expect it will eventually continue a historic trend of Venmo’s ‘copy-vation’, constantly playing catch-up chasing Cash App’s product releases. While not an exhaustive list, the below graphic shows Cash App’s major feature release velocity since 2015 and Venmo’s attempts to keep up.

User Obsession: The Core of Block’s Culture

As the consistent pace of product releases continues, Cash App will move closer to building a modern, consumer-first banking alternative and realising its vision of redefining the world’s relationship with money. In doing so, however, it runs the risk of overwhelming the user experience and becoming the very thing it is seeking to redefine: the unapproachable financial institution.

Here, we think Block’s cultural obsession with maximising the customer experience will be the defining characteristic of its ongoing success.

Historically there have been multiple evolutions of Cash App’s navigational architecture aimed at unburying features previously lost by bringing them closer to the surface and optimising for a more intuitive user flow. For example, its ‘direct deposit’ feature saw a 57% lift in usage post its most recent navigation redesign.

In contrast, Venmo has stuck with its public user transaction social feeds as it believes the feature defines it as a social network. Described by many commentators as ‘creepy’ and historically scrutinised by regulators for user privacy shortcomings, Venmo did not close its global feed or give users the ability to set privacy settings for their friend’s lists until 2021. Even today, transactions are still public-by-default to friends circles.

It’s understood that around 40% of Venmo users have manually switched transactions to private, and there are likely many more who would but don’t know how. The campaigning by users and industry bodies to encourage Venmo to clean up its privacy act, and the significant proportion of users manually changing their privacy settings, indicates a lack of customer obsession.

It’s Not Over Yet

Leveraging lessons from Square’s growth playbook, such as the importance of a customer obsession combined with a creative go-to-market, Cash App has turned into a US consumer finance powerhouse — 80 million annual users and the #1 ranked finance app across the Google and Apple app stores since 2017.

Despite its historic success, we think the most exciting part of Cash App’s journey lies ahead. In part three, we explore the opportunity ahead as Block converges it networks through the introduction of Cash App Commerce.

The article has been prepared by ECP Asset Management Pty Ltd (ECP). ECP is a funds management firm based in Sydney, Australia. For further information, visit www.ecpam.com. ECP and the author own shares in Block (ASX: SQ2). This material has been prepared for informational purposes only and is not intended to provide and should not be relied on for financial advice. ECP and the analyst own shares in CSL Ltd. ABN 26 158 827 582, AFSL 421704, CAR 441986.

Featured Articles